Announcing Matrix XII: An $800M fund to invest from concept to Series A Read more

I recently wrote about ghost markets and used B2B payments as an example. I got a lot of questions about that, so I wrote this to explain (1) why B2B payments is a ghost market and (2) where opportunities actually exist with B2B payments.

If you missed the ghost markets piece, the TLDR is: ghost markets are those that seem attractive, but are actually defined so broadly, or so narrowly, that it dooms the startup.

B2B payments is a ghost market because everyone focuses on the “payments” part of it. This is understandable because it has the hallmarks of a great startup opportunity: tons of activity (>$100 trillion annually!) and an antiquated status quo (42% via check and cash, 41% ACH, and 11% wires… yikes!). But this size distracts from the real problems and opportunities.

The misconception is that payments are a problem in B2B payments. They’re not a problem, or at least not the problem. What’s hardest, most broken, and ultimately most valuable in B2B payments? The workflows and data that are the precursor to the payment being made.

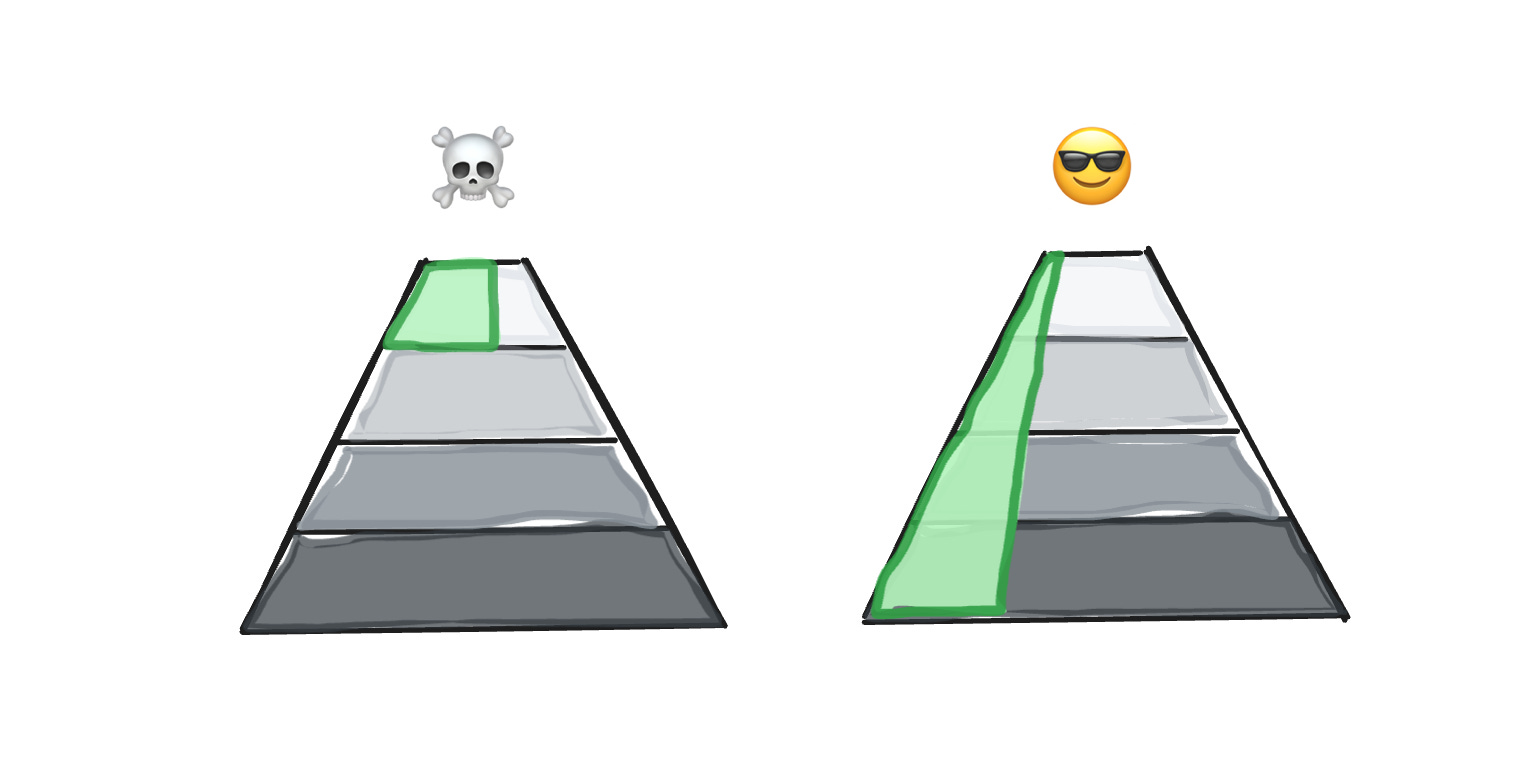

I think of the B2B payments as something like Maslow's Hierarchy of Needs: each layer is important in its own way, but you can’t focus on one unless you’ve solved the one below it. E.g., you can’t self-actualize if you’re starving or not physically safe.

In B2B payments, various operational workflows are the foundation of the pyramid, and the actual money movement is it the top. It’s an important part of the overall pyramid, but relies on all the layers below it.

Using this visualization, think of “B2B payments” as a ghost market when defined as the green shaded area on the left below. Conversely, if you focus less on the payments as an end in themselves, and instead view payments as the end of a specific B2B workflow that can be owned end-to-end, that’s a much more tractable approach.

Businesses have historically had access to many good enough options to accept and spend money. They may wish the fees were lower or settlement faster, but the market has been reasonably efficient in driving non-cash acceptance over the last few years.

Each market will have its own unique data model (discussed here in the context of vertical ERPs), workflows, and adjacent software products that precede the actual payment. However, a few common steps and challenges that precede a payment can include:

Only then can the actual payment be made. While the actual release and acceptance of payment is a common denominator across multiple industries, the complex steps described above vary widely by industry. So a simply stating that you make it easy for businesses to pay and get paid misses the problem.

If the problem isn’t in the payments but the workflows, then the most interesting implication is that the most successful “B2B payments” companies won’t look like payments companies at all.

Here are some markets and companies within them that are approaching the problem correctly, not as “B2B payments”, but as a workflow and data problem. By solving that, they earn the right to absorb the underlying payments of those businesses.

Freight auditing and payment: freight is a large part of every good’s cost and so a large part of an economy’s overall spend. Carriers are paid (and fined) based on a complex set of factors agreed upon before shipping and that can change before, during, and after the shipment itself. These range from the simple (like the average cost of gas) to the more complex (like fees and fines for tolls, overtime, being early or late, or taking too long to unload at a given destination).

There’s a large, mainly BPO-driven industry in freight audit and payment that helps (you guessed it) audit and then pay these invoices. The actual payment is straightforward, but decoding and verifying an invoice, with the industry’s esoteric coding and multiple supporting documents, is not. A product that can audit exceptionally faster, cheaper, and more accurately than alternatives, and then process the resulting payments, is likely way more attractive to a buyer than one that does the auditing poorly but the payments much better in some way. See Loop as an example here.

Construction supply chain: this is a massive market in the US and internationally, as general and subcontractors buy everything from concrete and lumber to windows, doors, and appliances from tens of thousands of retailers. These retailers operate like many others, except in the critical area of taxes. There’s a highly specific set of taxes that apply to construction materials based on who’s buying them, what kind of project they’re used for (home vs. office building vs. hospital), where they’re used, and so on. The same item can have different tax rates, even if it's sold to the same buyer! The retailer is responsible for calculating, verifying, and collecting these SKU-specific taxes before payment. Today this is often a manual process, but companies like Nickel help to automate it along with the payment itself.

Fuel cards: this is another massive category where the payment itself may seem trivial, but the industry-specific workflows and validations around the payment are critical and valuable. Truckers spend a significant amount on fuel and other relevant expenses (such as maintenance and tolls). However, simply giving drivers a payment card, even one with limits, doesn’t prevent them from buying unapproved items, buying overpriced fuel, filling up personal vehicles, or improperly accounting for expenses.

Incumbents like Wex and Fleetcor, as well as newer companies like Mudflap, AtoB, and Coast make it easy for vehicle fleets to find inexpensive fuel while getting control over and transparency into the spend.

If B2B payments, defined as such, is a ghost market, where are the real opportunities? Here are some quick thoughts.

It seems to me that the real opportunity is in vertical ERPs, which is another way of saying SaaS-first B2B payments. The playbook is to build a series of interlocking SaaS products that own steps of the workflow that precede a payment, and then work your way up the pyramid until you own the payment itself.

Thinking about B2B payments this way pairs well with one of my favorite pieces of writing from this year, “Subtle Differentiation (or why there are no 10x products in fintech)”. The headline gives away the key point: that it’s very hard to build 10x better products in fintech. This is especially true in B2B fintech, where businesses generally have good enough, cheap enough, fast enough financial products. However, if you view B2B payments not just as a payment problem, but one at the end of a string of workflows, it creates more surface area to actually create a 10x solution by improving the preceding workflows rather than being limited to the payment itself.